Cost of Sales Formula for Trading Company

Outline

By the term Cost of Sales, we usually mean the direct cost which has been incurred to bring the sales.

This typically includes direct purchase cost, direct material cost, direct labour cost or any other direct cost incurred for earning the sales.

Calculation of cost of sales is important as without it we’ll not know how much gross profit we earned (or how much gross loss we incurred) from the sales.

However, if we try to calculate the cost of sales directly (without any formula), it would be extremely difficult.

We’ll have to manually keep a track of each cost of each sale, and then at the end of the period, add up all those costs to arrive at total cost of sales.

But this method can be cumbersome and practically, impractical.

Therefore, some wise people put their heads together and came up with a simple formula to calculate the cost of sales.

If we’ve the answer to the components of this formula, we can calculate cost of sales relatively easier.

Let’s explore what is the formula to calculate cost of sales, for a trading company.

Formula for Cost of Sales calculation

There are three components of calculating cost of sales amount.

If they get to know all 3 of them, the final calculation of cost of sales would be a piece of cake, especially for a trading company.

Please note that all the components in the above formula need to be taken in amounts i.e., in the currency values and not in the quantities.

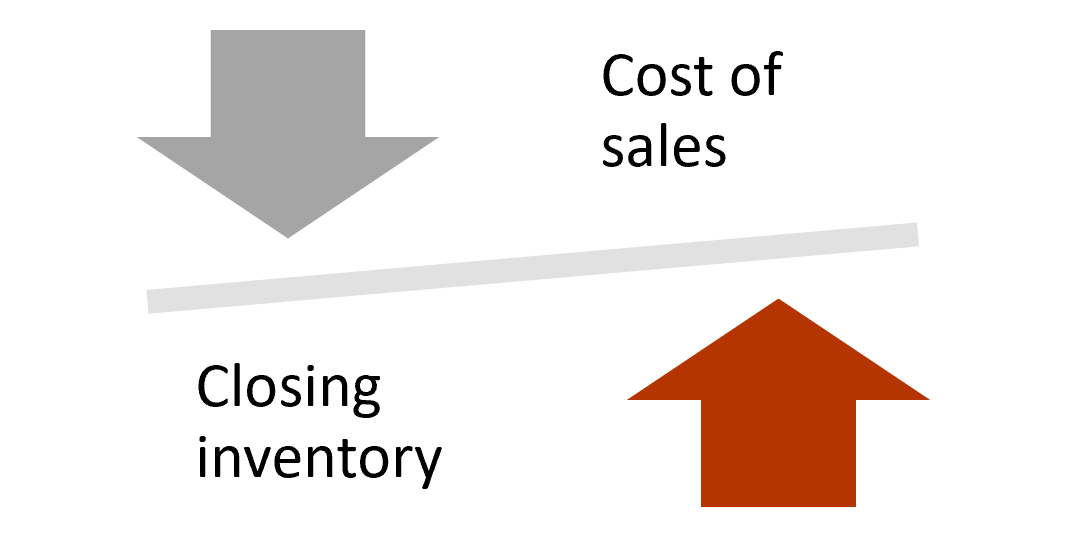

This formula effectively means that the higher the closing stock valuation, the lower will be the cost of sales.

The three components in the above formula have been given in the order of easiness.

It is easiest to calculate opening inventory value, little more effort is required for purchases and the most challenging is finding the valuation of closing inventory.

Let’s explore them one by one.

Formula for calculation of opening inventory amount

What is opening inventory?

The opening inventory means the inventory at the beginning of the current accounting period.

If we’re starting our books on 1 January of the year, then the opening inventory amount will be the same as inventory valuation in our stocks as at 1 January morning.

This would ideally be the same inventory which was last year’s night i.e., 31 December closing.

Opening inventory value in current accounting period = closing inventory of the previous accounting period

So, if we are starting a new business, most likely our opening inventory items will be zero at the beginning of our first accounting period.

If we are in a running business, the value of our opening inventory will be same as the value of closing inventory of last accounting period.

Formula for calculation of purchases during the period

The purchases during the period are equivalent to all the inventory items purchased during the period, simple.

So, let’s say that we started our business on January 1st and purchased few items as per below schedule.

So, in this case, our opening inventory will be zero (as the closing inventory of previous period was zero).

Our purchases quantity will be sum of all the purchases during January i.e., 50 units.

The value of all the purchases will be sum of all the invoices our suppliers charged us, which in this case is $245.

Formula for valuation of closing inventory

Valuation of closing inventory is the most intriguing section in the calculation of cost of sales.

Cost of Closing inventory = Quantity × Per unit cost

Let’s first understand what the challenges in valuation of closing inventories are.

Do we know the quantity of closing inventories?

This problem can be solved by physically counting the inventories.

Do we know the per unit cost of closing inventories?

This can be a challenge because the purchase prices cannot be seen physically on the closing inventory.

Can’t we check this from the invoices of our suppliers?

Yes, we can check, but there are additional challenges.

Let’s say we purchased 100 units from Supplier A at a rate of $5 and another 50 units from Supplier B at a rate of $6.

Now, out of these 150 units, we’ve sold 80 units to our customers.

The units which were sold were mix of products purchased from supplier A and supplier B.

Now, we need to find out how much of the remaining closing stock of 70 units belongs to Supplier A and how many are of supplier B.

Manually finding out one by one which closing items belonged to which rate is not recommended.

It might be practically cumbersome or extremely difficult to find this in case of large businesses.

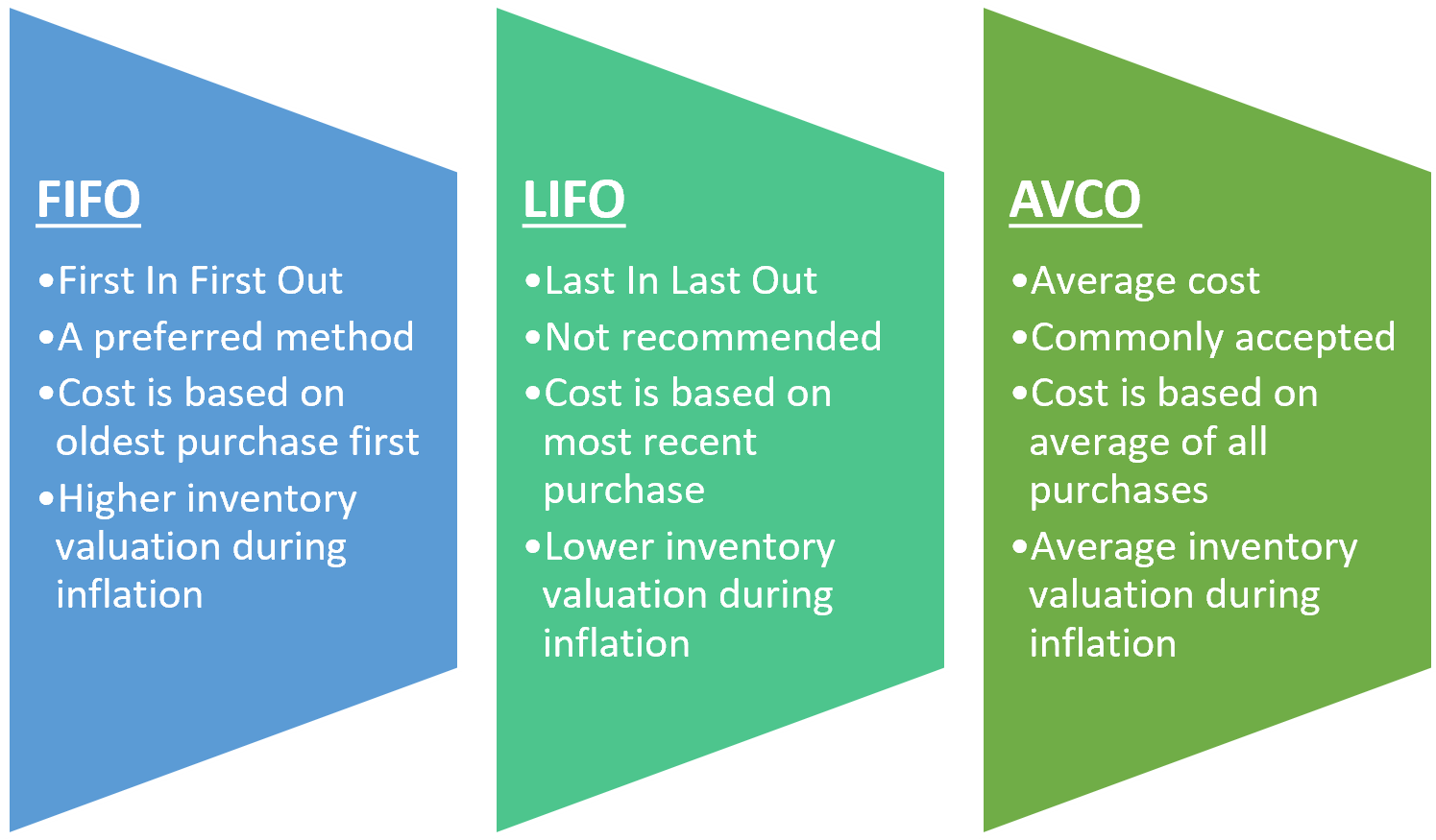

So, to value closing inventories, three types of policies were designed.

First in First Out basis of closing inventories valuation

The assumption that the out-going inventory is the one which is first purchased will go out first.

So, based on the dates of the purchases, we can find out the first received inventory has been sold and the most recently received inventory is lying in the warehouse.

Last in First Out basis of closing inventories valuation

Under this policy, we assume that the most recently purchased inventory has been sold first. So, the remaining closing inventory on hand is the oldest possible item purchased.

Average costing method of closing inventory valuation

This method assumes that the items which are currently lying on the floor are neither firstly purchased nor lastly purchased, instead, these are mix of both.

Therefore, under this method, we value the closing inventory at the average prices.

Practical case study of closing inventory valuation and cost of sales calculation (full example)

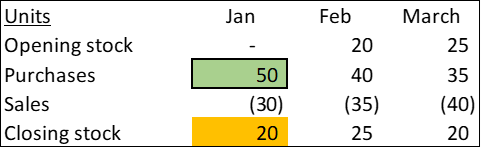

Take example of a trading business which purchased 50 fans during the January month and sold 30 units out of these. Now it has remaining 20 units in hand of closing inventory at hand.

Our objective is to find out the value of these 20 units of the closing inventory, so that we can calculate correct cost of sales of 30 units sold.

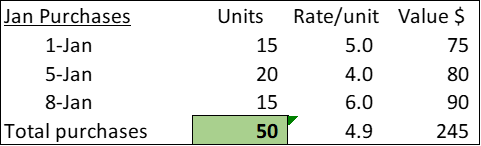

The starting point for us is to find out purchase costs of the 50 units procured during the period.

To value closing inventory, there are 3 generally discussed methods: FIFO, LIFO and AVCO.

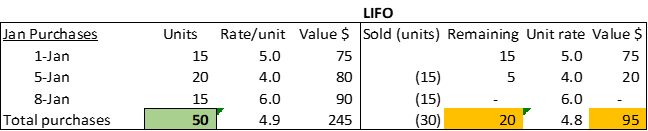

LIFO method valuation of closing inventory

Taking the same example, we know that we had inventory purchased on 3 different dates in January.

Now the sold items will be assumed to have been sold from the most recently purchased items.

This way, our total sale of 30 units will be completed from 15 units of 8 January purchases and remaining 15 units of January 5th purchased.

So, the closing inventory will be comprised of all 15 units of January 1st purchased + remaining 5 units of 5th January purchases.

This way, our closing inventory is valued at $95 for 20 units.

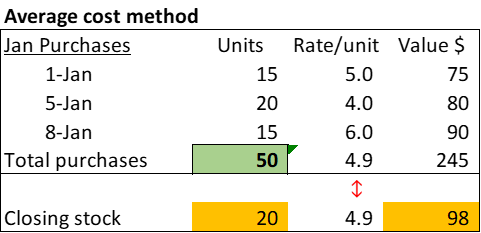

AVCO method valuation of closing inventory

This method assumes that closing inventory should be valued at the average of all the purchases during the period.

In this example, we added up all the units reaching at 50 units and added all the cost which is $245. So, by dividing $245 with 50 units, we arrived at average of $4.9/unit.

The closing inventory of 20 units will be valued at $4.9/unit resulting in a valuation of $98.

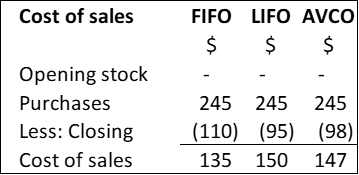

Cost of Sales calculation using all three methods (FIFO, LIFO, AVCO)

Now, we’ve calculated closing inventory values under all three methods.

FIFO results in the highest closing inventory value, resulting in lowest cost of sales.

LIFO results in the lowest closing inventory value, resulting in highest cost of sales.

AVCO results in a middle-ground valuation.

Which inventory valuation method is best?

LIFO is generally not accepted under GAAP.

FIFO makes sense chronologically.

AVCO is often the most practical and balanced.

Formula for cost of goods sold (COGS) in a service organization

A service organization does not buy inventory for trading.

Therefore, cost of sales includes:

- Direct staff charges

- Directly attributable expenses

Formula for cost of goods sold (COGS) in a manufacturing company

Cost of Sales = Opening Stock + Cost of Goods Manufactured – Closing Stock

Formula for Cost of Goods Manufactured (COGM)

COGM = Direct Materials + Direct Labour + Production Overheads

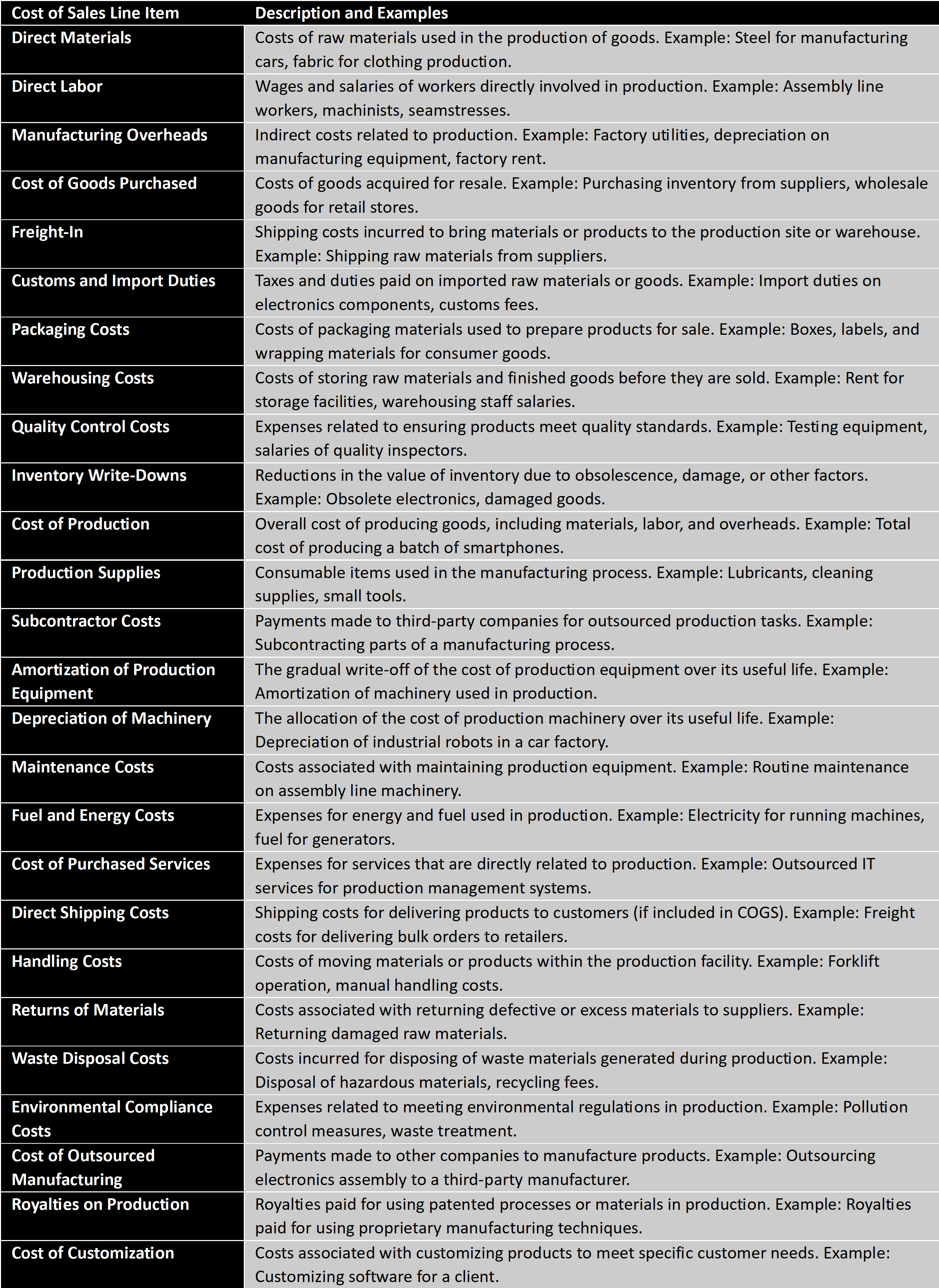

Production overheads include utilities, depreciation, rent, shipping, duties, packaging, storage, testing, damage, waste disposal, outsourced manufacturing, customization, etc.

Cost of Goods Sold Margin Calculation Formula

Cost of Sales margin = (Cost of Sales / Sales) × 100

Examples of what cost of sales includes

Cost of sales includes direct materials, direct labour, overheads, freight-in, duties, packaging, warehousing, quality control, write-downs, production supplies, subcontract costs, depreciation, fuel, energy, shipping, handling, returns, waste disposal, environmental compliance, outsourced manufacturing, royalties, and customization.